The Classical Linear Regression Model (CLRM) is the foundation of econometrics. It ensures that Ordinary Least Squares (OLS) estimators are BLUE — Best Linear Unbiased Estimators. For this to hold true, certain assumptions must be satisfied. Let’s explore them step by step.

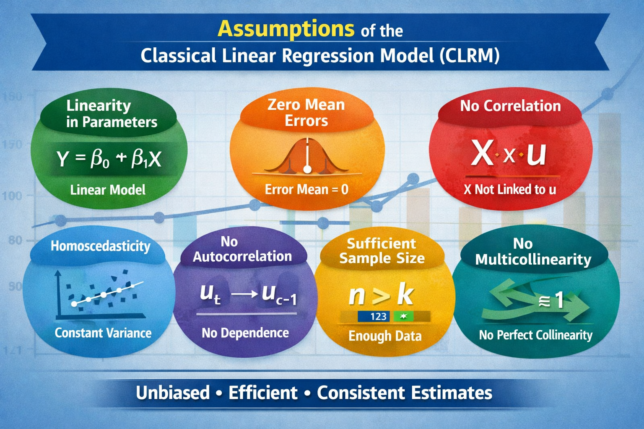

1. Linearity in Parameters

- Meaning: The regression equation must be linear in coefficients.

- Example: Y=β0+β1X+u is linear. Even if X2 is included, the model remains linear in parameters.

- Violation: Y=β0+β12X+u is nonlinear in parameters → OLS cannot be applied.

2. Zero Mean of Error Term

- Meaning: The expected value of the error term is zero: E(u∣X)=0.

- Example: If a wage model consistently underpredicts by ₹500, the error mean ≠ 0.

- Violation: Estimates become biased.

3. No Correlation Between Regressors and Error Term

- Meaning: Independent variables must not be correlated with the error term.

- Example: In studying wages, if ability (unobserved) affects both education and wages, then education is correlated with the error.

- Violation: Endogeneity → biased and inconsistent estimates.

4. Homoscedasticity (Constant Variance of Errors)

- Meaning: Error variance must be constant across all values of X.

- Example: If income regressions show larger error variance at higher income levels, heteroscedasticity exists.

- Violation: Standard errors become unreliable → hypothesis tests invalid.

5. No Autocorrelation

- Meaning: Error terms must be independent across observations.

- Example: In inflation time series, today’s error should not depend on yesterday’s.

- Violation: Inefficient estimates and misleading test statistics.

6. Sufficient Sample Size

- Meaning: The number of observations must exceed the number of parameters.

- Example: Estimating two parameters requires at least three data points.

- Violation: Regression cannot be computed.

7. No Perfect Multicollinearity

- Meaning: Independent variables must not be perfectly correlated.

- Example: If income and expenditure are perfectly correlated, OLS cannot separate their effects.

- Violation: Regression collapses.

Why These Assumptions Matter

Bias: Wrong estimates (e.g., omitted variable bias).

Inefficiency: Less precise estimates (heteroscedasticity, autocorrelation).

Invalid Inference: Hypothesis tests unreliable.

Econometricians use diagnostic tests like Durbin‑Watson (autocorrelation), Breusch‑Pagan (heteroscedasticity), and VIF (multicollinearity) to check violations and apply remedies such as robust standard errors, GLS, or instrumental variables.

Conclusion

Understanding CLRM assumptions is essential for anyone learning econometrics. By mastering these foundations, you can confidently apply regression analysis to real‑world data and avoid common pitfalls in statistical modeling.